How long does car finance approval take? Generally, car loan approval can take anywhere from a few minutes to a few business days, depending on the lender, your financial situation, and the type of loan.

Securing a car loan is a crucial step in the car buying journey. Many buyers wonder about the car loan waiting time and how quickly they can get behind the wheel of their new vehicle. The auto loan approval speed can vary significantly, impacting the overall financing car turnaround time. This comprehensive guide aims to demystify the loan decision time for car financing, covering the entire car financing process duration and what influences it. We’ll explore how long it takes to get a car loan and the factors that can speed up or slow down your car purchase financing timeline.

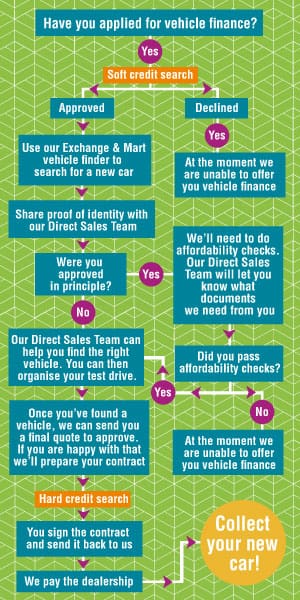

Image Source: www.moneybarn.com

The Speed of Auto Loan Approval: Key Influencing Factors

Several elements play a role in determining the speed of auto loan approval. Understanding these can help you prepare and potentially expedite the process.

1. Your Credit Score and History

Your credit score is a primary determinant of how quickly you can get approved for a car loan. Lenders use your credit score to assess your risk as a borrower.

- Excellent Credit (720+): If you have a strong credit history with a high score, you are likely to experience very fast approval. Many lenders offer instant or near-instant approvals for borrowers with excellent credit. This is because they are seen as low-risk.

- Good Credit (670-719): Approval times are still generally quick, often within a few hours to one business day.

- Fair Credit (580-669): You might experience a slightly longer approval process as lenders may need more time to review your financial details. Expect this to take a day or two.

- Poor Credit (Below 580): Approval can take longer, sometimes several business days, and may involve more scrutiny. You might also be directed to specialist lenders.

Credit History Length: A longer credit history, showing responsible borrowing over time, is generally viewed favorably and can contribute to faster approvals.

Credit Report Accuracy: Ensure your credit report is accurate. Errors can cause delays or rejections.

2. Type of Lender

The type of institution you apply with can significantly affect the car loan application processing time.

- Dealership Financing: Often the fastest option. Dealerships work with multiple lenders and can submit applications to several at once. They often have streamlined processes designed for quick sales. This can lead to very rapid approval, sometimes within minutes.

- Banks and Credit Unions: Traditional financial institutions can be a bit slower. While they offer competitive rates, their car financing process duration might involve more in-depth manual review. Approval can take anywhere from a few hours to a couple of business days. Credit unions, in particular, are known for their customer service and may offer quick turnaround times, especially for existing members.

- Online Lenders: Many online lenders specialize in auto loans and have highly automated systems. This can result in very fast approvals, often within minutes or hours, especially for pre-qualification. The final approval might take a bit longer as they verify all documentation.

- Subprime Lenders: Lenders who specialize in working with borrowers with lower credit scores often have a longer car loan application processing time. They need to conduct more thorough checks due to the higher risk involved.

3. Loan Application Completeness and Accuracy

A complete and accurate application is critical for speeding up the car loan waiting time.

- Missing Information: If you fail to provide all the necessary documents or information, the lender will have to follow up with you, adding days to the process.

- Inaccurate Details: Errors in your income, employment history, or personal details can trigger a manual review, slowing down the loan decision time.

4. Required Documentation

The more documentation you can provide upfront, the smoother and faster the approval process will be. Common documents include:

- Proof of income (pay stubs, tax returns)

- Proof of employment (employer contact information)

- Proof of address (utility bills, lease agreement)

- Driver’s license or other government-issued ID

- Information about the vehicle you wish to purchase (VIN, purchase price)

- Proof of insurance

Having these readily available can significantly reduce the time to get car loan.

5. Loan Amount and Vehicle Value

The amount you are borrowing and the value of the car can also play a role.

- Larger Loan Amounts: Loans for higher amounts might require more thorough underwriting, potentially extending the approval time.

- New vs. Used Cars: Financing a new car might be slightly quicker than a used car, as the vehicle’s value is more easily determined by the lender. However, this difference is often minimal.

- Specialty Vehicles: Financing for classic cars, exotic cars, or vehicles with unique circumstances might take longer due to valuation complexities.

6. Time of Application and Business Days

Lenders have business hours. Applying on a Friday afternoon or just before a public holiday can mean waiting until the next business day for processing, increasing the car purchase financing timeline.

The Car Financing Process Duration: Step-by-Step Breakdown

Let’s break down the typical car financing process duration from application to approval.

Step 1: Pre-Qualification/Pre-Approval (Optional but Recommended)

- What it is: A preliminary check of your creditworthiness.

- How long it takes: Can be instant online, often with a soft credit check that doesn’t impact your credit score.

- Benefit: Gives you an idea of loan amounts and rates you might qualify for, and helps you shop with confidence. This is a great way to get a sense of the speed of auto loan approval without committing.

Step 2: Completing the Loan Application

- What it is: Filling out the formal loan application with all required personal, employment, and financial information.

- How long it takes: Can take 15-30 minutes to complete online or in person. The accuracy and completeness here directly impact car loan application processing.

Step 3: Lender Underwriting and Verification

- What it is: The lender reviews your application, verifies your information, checks your credit report, and assesses your ability to repay the loan. This is where the core loan decision time happens.

- How long it takes: This is the most variable part.

- Quick Approvals (Minutes to Hours): For borrowers with excellent credit applying through online lenders or dealerships with automated systems.

- Standard Approvals (1-2 Business Days): For most applicants with good to fair credit applying through banks, credit unions, or dealerships.

- Extended Approvals (2-5+ Business Days): For applicants with lower credit scores, complex financial situations, or those applying for less common vehicle types. This extended car loan waiting time is due to the deeper review required.

Step 4: Loan Offer and Review

- What it is: If approved, the lender presents you with the loan terms (interest rate, loan term, monthly payment).

- How long it takes: Typically issued immediately after underwriting is complete. You then have time to review the offer.

Step 5: Finalizing the Loan and Vehicle Purchase

- What it is: You accept the loan terms, sign the loan agreement, and finalize the purchase of the vehicle.

- How long it takes: Often completed on the same day as approval, especially at a dealership. If you’re applying independently, this might take another business day.

Strategies to Expedite Your Car Loan Approval

Want to shorten the car financing process duration? Here are some strategies:

1. Get Pre-Approved Before Shopping

- Why it works: Knowing your budget and approved loan amount beforehand allows you to focus your car search and negotiate from a stronger position. It also means a significant part of the car purchase financing timeline is already completed.

- How to do it: Apply for pre-approval with your bank, credit union, or a reputable online lender before visiting a dealership.

2. Improve Your Credit Score

- Why it works: A higher credit score is the single biggest factor in getting fast approval and better rates.

- How to do it:

- Pay all bills on time.

- Reduce credit utilization ratio.

- Dispute any errors on your credit report.

- Avoid opening new credit accounts just before applying for a car loan.

3. Organize Your Financial Documents

- Why it works: Having all necessary documents ready streamlines the lender’s verification process.

- What to gather:

- Recent pay stubs

- Last two years of tax returns (if self-employed or commission-based)

- Bank statements

- Proof of residence (utility bill, lease agreement)

- Valid driver’s license

- Insurance information

4. Choose the Right Lender for Your Situation

- Why it works: Some lenders are faster or better suited to your credit profile.

- How to do it:

- If you have excellent credit, compare offers from banks, credit unions, and online lenders.

- If you have fair or poor credit, consider specialist lenders or credit unions known for working with a wider range of applicants. Dealerships can also be a good starting point for these situations.

5. Be Prepared to Negotiate, But Don’t Delay Approval

- Why it works: While negotiating the car price is important, don’t let it unduly delay the financing approval itself.

- How to do it: Secure your financing approval first, then negotiate the car price. This ensures you can drive away in your new car promptly once the deal is struck.

What Happens If Your Car Loan Application is Delayed?

If your car loan application processing is taking longer than expected, here’s what might be happening and what you can do:

Potential Reasons for Delays

- Incomplete Information: The lender needs more details or documents from you.

- Credit Report Issues: The lender is verifying information on your credit report or found something unexpected.

- High Application Volume: The lender is experiencing a surge in applications, slowing down their car financing process duration.

- Complex Financial Situation: You have multiple streams of income, are self-employed, or have other financial complexities that require more thorough review.

- Vehicle Eligibility: The car you want to finance might not meet the lender’s criteria (e.g., age, mileage, special type).

What You Can Do

- Contact the Lender: Reach out to your loan officer or the lender directly. Ask for an update on your loan decision time and inquire if any additional information is needed.

- Provide Information Promptly: If the lender requests more documents or clarification, provide it as quickly as possible to avoid further delays.

- Check Your Credit Report: Ensure there are no errors that could be causing the hold-up.

- Consider Alternatives: If the delay is significant, you might want to explore other lenders to compare auto loan approval speed and terms.

Frequently Asked Questions About Car Finance Approval Time

Q1: Can I get a car loan the same day I apply?

A1: Yes, it’s possible, especially if you have excellent credit and apply through a dealership or an online lender with a fast, automated system. This significantly shortens the time to get car loan.

Q2: How long does it take for a bank to approve a car loan?

A2: For banks, the car financing process duration typically ranges from a few hours to 1-2 business days, depending on your creditworthiness and the completeness of your application.

Q3: Does applying at multiple dealerships affect my approval time?

A3: While applying at multiple dealerships might seem like it could speed things up, it’s generally better to get pre-approved with one lender first. Multiple hard credit inquiries in a short period can slightly impact your credit score, though they are often grouped together by credit bureaus.

Q4: How long is a car loan approval valid for?

A4: This varies by lender, but pre-approvals are often valid for 30 to 90 days. The actual loan offer, once finalized, might have its own validity period.

Q5: What is the quickest way to get approved for a car loan?

A5: The quickest way involves having a strong credit score, gathering all necessary documents beforehand, getting pre-approved by a fast lender (like an online lender or credit union), and ensuring your application is complete and accurate. This approach maximizes your chances for a swift auto loan approval speed.

Q6: How long does it take for a car loan to be funded?

A6: Once approved and you’ve signed the paperwork, funding typically happens very quickly. At a dealership, it’s often the same day. If you applied independently, it might take 1-2 business days for the funds to be disbursed.

Q7: Does the type of car affect how long it takes to get approved?

A7: Generally, financing for new or widely available used cars is quicker. Unique vehicles, like classic cars or those with very high values, might require more time for appraisals and lender review, extending the car loan waiting time.

In conclusion, while the time to get car loan can vary, understanding the factors involved and employing smart strategies can help you achieve a rapid car finance approval. By being prepared and informed, you can significantly shorten your car purchase financing timeline and get behind the wheel of your desired vehicle sooner.