Can you settle a car accident privately? Yes, in many cases, you can settle a car accident privately, especially for minor incidents where there are no serious injuries or significant property damage. This approach can help you avoid the complexities and delays often associated with insurance claims and legal processes.

Dealing with a car accident can be stressful. You might be wondering if there’s a simpler way to handle things than going through insurance companies. For many minor accidents, the answer is yes! Settling privately means you and the other driver (or drivers) involved agree on how to resolve the damages and costs without formal insurance claims or legal action. This can save time, reduce stress, and potentially avoid premium increases. This guide will walk you through how to achieve a private car accident resolution smoothly and efficiently.

Image Source: b2404211.smushcdn.com

Deciphering the Basics of Private Settlements

A private settlement for a car accident is a direct agreement between the parties involved. This means you and the other driver(s) discuss the damages, who is at fault, and how compensation will be handled. It’s a way to resolve the issue directly, often for fender-benders or situations with minimal damage.

When is Private Settlement a Good Idea?

There are specific situations where opting for a private resolution is often the best course of action:

- Minor Property Damage: If the damage to vehicles is cosmetic or easily repairable and the cost is relatively low, a private settlement can be efficient. Think of minor scrapes, bumper damage, or cracked taillights.

- No Injuries: This is a crucial factor. If no one involved sustained any injuries, even minor ones, private settlements become much more feasible and advisable. Personal injury claims add a layer of complexity due to medical bills, pain and suffering, and future care costs.

- Clear Liability: When fault is obvious and not disputed, it simplifies the negotiation process. For instance, if someone rear-ended you while you were stopped at a red light, liability is usually clear.

- Mutual Agreement: Both parties must be willing to discuss and agree on a settlement amount and method. If there’s significant disagreement or distrust, a private settlement might not be the right path.

- Avoiding Insurance Involvement: You might choose a private settlement to avoid reporting the accident to your insurance company. This is often done to prevent potential increases in your insurance premiums.

When to Avoid Private Settlements

While attractive, private settlements aren’t always suitable. You should involve insurance or legal professionals if:

- Serious Injuries: Any injury, no matter how minor it seems initially, can escalate. Medical costs can be high, and future complications can arise. Always err on the side of caution.

- Significant Property Damage: If repairs will be extensive or costly, it’s wise to involve insurance to ensure proper assessment and coverage.

- Disputed Liability: If there’s any doubt about who caused the accident, or if multiple parties are involved and fault is unclear, insurance or legal experts are needed to determine liability.

- Uninsured or Underinsured Drivers: If the at-fault driver has no insurance or insufficient coverage, a private settlement might be the only way to get compensation, but it carries risks.

- Complex Accidents: Accidents involving multiple vehicles, commercial vehicles, or hazardous materials require professional handling.

Steps to Negotiating a Private Car Accident Settlement

Successfully settling a car accident privately requires a calm, organized, and fair approach. Here’s a breakdown of the steps involved in negotiating car accident damages:

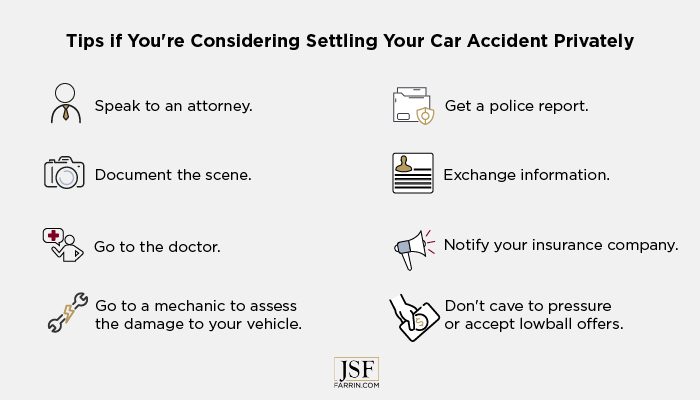

Step 1: Ensure Safety and Exchange Information

After ensuring everyone is safe and no one needs immediate medical attention, the first crucial step is to exchange information. This is vital even for a private settlement, as it provides a record and confirms identities.

- Contact Information: Get names, addresses, phone numbers, and email addresses.

- Insurance Information: Even if you plan to settle privately, collect the other driver’s insurance details. This can be useful later if unexpected issues arise.

- Vehicle Information: Note down the license plate number, make, model, and year of the other vehicle(s).

- Driver’s License: Verify the other driver’s license and note down their license number.

Step 2: Document the Scene

Thorough documentation is your best friend when negotiating car accident damages.

- Photos and Videos: Take pictures of the damage to all vehicles involved from multiple angles. Capture close-ups of the impact points and wider shots showing the vehicle positions. Also, photograph the surrounding area, road conditions, and any traffic signals or signs.

- Witness Information: If there were any witnesses, ask for their contact information. Their statements can be invaluable if disputes arise later.

- Accident Description: Write down your account of what happened as soon as possible while the details are fresh in your mind. Be factual and objective.

Step 3: Get Repair Estimates

To reach a fair out of pocket car accident settlement, you need to know the actual cost of repairs.

- Multiple Quotes: Obtain at least two or three repair estimates from reputable auto body shops. This helps ensure you’re getting a fair price and avoids overcharging or underestimating.

- Documentation: Keep all repair estimates, invoices, and receipts organized. If one party agrees to pay for repairs directly, these documents are essential for tracking costs.

Step 4: Determine Liability (If Not Clear)

Even in minor accidents, there can sometimes be a disagreement about fault.

- Review Evidence: Look at the scene photos, police reports (if any), and witness statements to assess who is likely at fault.

- Rules of the Road: Consider traffic laws relevant to your situation. For example, in most places, the driver who rear-ends another vehicle is presumed to be at fault.

- Disputing Car Accident Liability: If you believe the other driver is disputing car accident liability unfairly, refer back to your evidence. If a consensus cannot be reached, this is a strong indicator that a private settlement might not be the best route.

Step 5: Calculate Your Damages

Beyond vehicle repairs, consider all other costs you’ve incurred.

- Repair Costs: The agreed-upon cost from the body shop.

- Rental Car Costs: If you needed a rental while your car was being repaired.

- Lost Wages: If you missed work due to the accident or repairs.

- Other Expenses: Any other reasonable expenses directly related to the accident.

Step 6: Initiate Negotiations

Once you have all your information and estimates, you can approach the other party to discuss a settlement.

- Calm and Respectful Approach: Start the conversation calmly and professionally. State your intention to settle privately.

- Present Your Case: Clearly explain your assessment of the damages and liability, supported by your documentation and estimates.

- Listen Actively: Hear the other party’s perspective. They might have their own estimates or reasons for their position.

- Be Prepared to Compromise: A successful negotiation often involves some give and take. Aim for a resolution that both parties can accept.

- Avoid Emotional Arguments: Stick to the facts and the costs.

Step 7: Formalize the Agreement

Once you’ve reached an agreement on an amount, it’s crucial to formalize it.

- Car Accident Settlement Agreement: Draft a simple written agreement. This document should clearly state:

- The date and location of the accident.

- The names and contact information of all parties involved.

- The agreed-upon settlement amount.

- A statement that this settlement resolves all claims related to the accident.

- A release of all future liability for both parties concerning this specific accident.

- Signatures of all parties.

- Legal Release Form Car Accident: Ideally, this agreement should also function as a legal release form car accident. This form states that by accepting the settlement, both parties agree not to pursue any further legal action against each other regarding the accident. It’s a good practice to have an attorney review this document, especially if the settlement amount is significant.

Step 8: Payment and Exchange

Once the agreement is signed, arrange for payment.

- Payment Methods: This could be cash, a cashier’s check, or a personal check. Agree on a secure method.

- Proof of Payment: Get a receipt for the payment.

- Release of Claim: Once payment is made, the matter is considered closed according to your agreement.

Understanding the Financial Aspects of Private Settlements

Settling privately means you’re directly handling the financial consequences. This can involve paying for damages or receiving compensation.

Calculating Out-of-Pocket Costs

When you settle a minor car accident privately, you’re essentially calculating your out of pocket car accident settlement. This is the total amount you will pay or receive directly from the other party.

- Your Damages:

- Repair costs for your vehicle.

- Any medical expenses if you sustained minor injuries (though ideally, no injuries are present for private settlements).

- Rental car expenses.

- Lost wages.

- Other Party’s Damages:

- Repair costs for their vehicle.

- Any other documented expenses they incurred due to the accident.

Negotiating Car Accident Damages Fairly

The core of a private settlement is negotiating car accident damages. This involves finding a middle ground that both parties agree is fair.

Table: Common Damages in Minor Accidents

| Damage Type | Description | How to Assess |

|---|---|---|

| Vehicle Repairs | Cost to fix dents, scratches, broken lights, or other physical damage. | Obtain multiple repair estimates from reputable body shops. |

| Rental Car Fees | Cost of a temporary vehicle while yours is being repaired. | Keep rental receipts and check if the rental duration is reasonable for the repair timeline. |

| Diminished Value | The reduction in your car’s market value after an accident, even after repairs. | This is harder to quantify and often not included in simple private settlements. Usually addressed by insurance. |

| Lost Wages | Income lost due to missed work because of the accident or repairs. | Provide pay stubs or employer verification of missed workdays and earnings. |

Accident Claims Without Insurance

In rare cases, you might deal with accident claims without insurance. This typically happens when the at-fault party has no insurance and you agree to a private settlement. In such scenarios, you might accept a lesser amount than the full repair cost, or the at-fault driver might pay in installments. It’s crucial to have a written agreement clearly outlining the payment plan and the final resolution.

Potential Pitfalls and How to Avoid Them

While appealing, private settlements aren’t without risks. Being aware of these pitfalls can help you navigate them successfully.

Hidden Damages

Sometimes, the initial damage is obvious, but hidden problems are uncovered during repairs.

- Problem: A seemingly minor fender-bender could reveal structural damage, a bent frame, or damage to sensors not visible from the outside.

- Solution: If hidden damage is found after the initial agreement, you might need to reopen negotiations or, if the agreement was comprehensive, the at-fault party may be obligated to cover these costs. This is where a well-written car accident settlement agreement is crucial.

Unforeseen Injuries

Even without initial visible injuries, some can develop later due to the shock and stress of an accident.

- Problem: Whiplash or other soft tissue injuries may not manifest immediately but can lead to significant medical bills and pain and suffering.

- Solution: If injuries emerge after a private settlement, you may be barred from claiming further compensation if your legal release form car accident was too broad. This is a primary reason to avoid private settlements if there’s any doubt about injuries.

Disagreements After the Fact

Despite agreeing, disputes can still arise.

- Problem: One party might feel they paid too much, or the repairs weren’t done to their satisfaction.

- Solution: A clear, signed car accident settlement agreement with a release of liability is your best defense. It should explicitly state that the settlement is final and all claims are resolved.

Difficulty Collecting Payment

The at-fault driver might agree to pay but then delay or refuse to do so.

- Problem: You’ve handed over your car keys for repair, or they’ve promised payment, but it never materializes.

- Solution: This is where collecting insurance information is critical. If the other party defaults, you might have to go through your own insurance (if you have collision coverage) or pursue legal action, which defeats the purpose of a private settlement.

When Legal Counsel is Advisable

While this guide focuses on private settlements, there are times when seeking professional advice is essential.

Seeking Advice for a Personal Injury Settlement

If your accident involves any injury, it’s almost always best to consult with a personal injury lawyer. They can help you:

- Assess the Full Value of Your Claim: This includes not only medical bills but also pain and suffering, lost earning capacity, and other damages.

- Negotiate with Insurance Companies: Lawyers have experience dealing with adjusters and can often secure a better personal injury settlement than an individual.

- Understand Legal Release Forms: They can ensure you don’t sign away rights you may not realize you have.

Navigating Complex Liability Disputes

If you are disputing car accident liability or if the circumstances are complex, a lawyer can be invaluable. They can help gather evidence, understand legal precedents, and represent your interests in discussions or potentially in court.

Conclusion: Weighing the Pros and Cons

Settling a car accident privately can be a straightforward and efficient way to resolve minor incidents. It saves time, avoids potential premium hikes, and offers a sense of control. However, it requires clear communication, careful documentation, and a willingness to compromise.

For minor incidents with no injuries and clear liability, a private car accident resolution can be ideal. Always ensure that you have a well-documented agreement, ideally including a comprehensive legal release form car accident, to protect yourself. Remember, the goal is a fair and final resolution that allows everyone to move forward without lingering disputes. If there are any injuries or significant damages, or if liability is unclear, it’s safer to involve your insurance company or seek legal counsel to ensure your rights are protected and you receive fair compensation.

Frequently Asked Questions (FAQ)

Q1: What if the other driver doesn’t have insurance?

If the at-fault driver has no insurance and you wish to settle privately, you’ll be dealing with accident claims without insurance. In this case, you can still present your estimate for damages and negotiate a payment. However, collecting the money could be challenging. You might agree on a payment plan, or the other driver might offer a lump sum. It’s crucial to get a written agreement and potentially a promissory note. If they fail to pay, your options for recourse might be limited without involving the legal system.

Q2: Do I have to report a minor accident to my insurance company if I settle privately?

In many jurisdictions, you are legally required to report any accident to your insurance company, regardless of fault or whether you settle privately. However, if the accident is very minor (e.g., no injuries, minimal damage that you are covering out-of-pocket), some people choose not to report it to avoid potential premium increases. This decision carries risk. If the other party later decides to file a claim or if unforeseen issues arise, your failure to report could impact your coverage. It’s best to check your policy and local regulations.

Q3: Can I get compensation for my car’s diminished value in a private settlement?

It’s difficult to get compensation for diminished value in a private settlement, especially for minor accidents. Diminished value refers to the loss of market value your car experiences after being involved in an accident, even if it’s perfectly repaired. Insurance companies typically handle these claims. In a private settlement, you would usually focus on the direct costs of repair. If your car is relatively new and high-value, the loss of value can be significant, and you might need to involve your insurance or a legal professional to pursue this.

Q4: What should I do if the other driver offers a very low settlement amount?

If the other driver offers a settlement that seems unreasonably low, don’t feel pressured to accept it. Calmly present your repair estimates and a breakdown of your damages. If they are unwilling to negotiate fairly or are disputing car accident liability without good reason, you may need to reconsider a private settlement and explore other options, such as filing an insurance claim.

Q5: Is a handwritten agreement enough for a private car accident settlement?

A handwritten agreement can be sufficient if it clearly outlines all the necessary details and is signed by all parties. However, it’s always better to type it out or use a template for clarity and professionalism. Ensure it functions as a legal release form car accident and explicitly states that both parties are settling all claims related to the incident.

Q6: What if I need to file a claim later after a private settlement?

Once you sign a comprehensive car accident settlement agreement that includes a release of liability, you generally cannot file a claim or sue the other party for anything related to that accident. This is why it’s crucial to be certain about the extent of your damages and injuries before agreeing to a private settlement and signing any documents.

Q7: How do I calculate lost wages for a private settlement?

To calculate lost wages, you need to determine how many days you missed work due to the accident or repairs and multiply that by your daily or hourly rate. You should have documentation, such as pay stubs or a letter from your employer, to verify your earnings and the time missed. This is a common component when negotiating car accident damages.